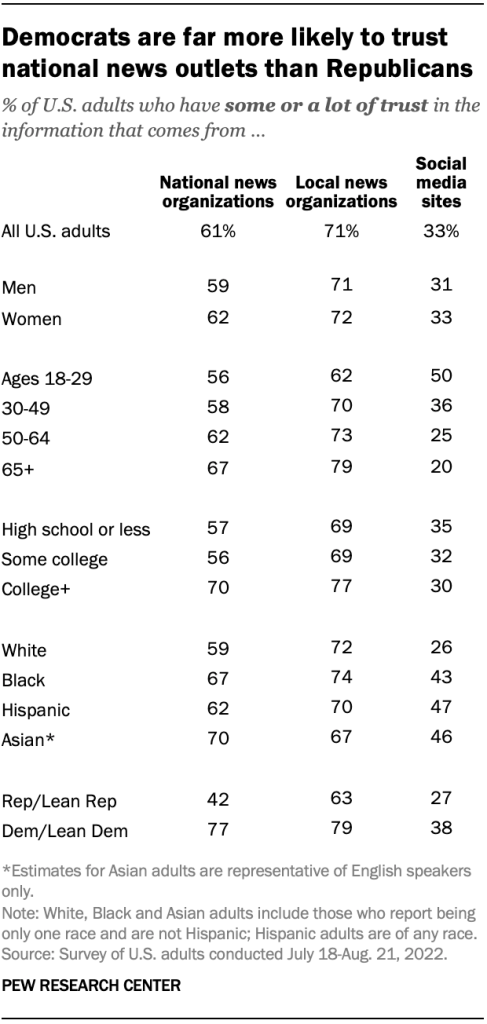

Trust is scarce in our modern times. Only about 20% of Americans trust our government, down from 77% in 1965. In addition, just 61% of Americans trust what they see on the national news and 33% trust what they read on social media. These aren’t shocking numbers, anyone could probably have inferred similar results right? All you need to do is take anecdotal evidence anywhere from our juvenile-behaving politicians to media members seemingly bidding their opinions to those with the deepest pockets.

{kind=link}

Curiously though, banks have been left somewhat unscathed from this erosion of trust. Greater than 80% of consumers worldwide completely or mostly trust their primary financial provider, according to Ernst & Young. I refer to this as curious because of behavior like this from the world’s largest banks such as Wells Fargo. Some highlights from the $3.7 billion fine levied upon Wells Fargo:

“Wells Fargo had systematic failures in its servicing of automobile loans that resulted in $1.3 billion in harm across more than 11 million accounts. The bank incorrectly applied borrowers’ payments, improperly charged fees and interest, and wrongfully repossessed borrowers’ vehicles.”

“For years, Wells Fargo unfairly charged surprise overdraft fees - fees charged even though consumers had enough money in their account to cover the transaction at the time the bank authorized it - on debit card transactions and ATM withdrawals.”

And if you didn’t know, this is not Wells Fargo’s first rodeo:

“Wells Fargo is a repeat offender that has been the subject of multiple enforcement actions by the CFPB and other regulators for violations across its lines of business, including faulty student loan servicing, mortgage kickbacks, fake accounts, and harmful auto loan practices.”

Just to give fair treatment to Wells Fargo and to show it isn’t just a firm-specific wrongdoing, here are examples from Citibank wiring $900 million to the wrong account and losing the money, Goldman Sachs being fined $2.9 billion for its involvement in a Malaysian bribery scheme, Bank of America being fined $225 million for botching unemployment disbursements during the height of pandemic, and an example industry-wide for attempting to skirt record-keeping laws by communicating on personal devices. By the way, these are just fines from the past two years. I could go back decades, even centuries to show again and again missteps and malfeasance from those we trust to hold and manage our money.

Bitcoin was born out of the 2008-09 financial crisis (again caused by banks), and is designed as a “trustless” payment system, or without needing financial intermediaries. This is a wonderful notion that is great in theory and some applications, however has not yet developed fully and still a financial product in its infancy. Even in the cryptocurrency space, one hailed as “trustless”, many entrepreneurs have founded successful businesses on the back of this system and act as financial intermediaries for their customers. Basically banks without the name banks. The point being is there is still a lot of human involvement in the system, which means there is likely to be fraud and corruption.

Did you know that banks are only required by the Federal Reserve to hold 10% of their deposits in reserve at any one time? This may come as a shocker to some, but if there was a bank run, there is no chance we would all get our money out.

A lot of bank proponents like to hide behind that all depositors have FDIC insurance, which is true and a great thing. (This means if there ever was a bank run, all depositors could get their funds because the bank has insurance - the FDIC is funded by the federal government and would give the depositors their cash.) However, two big problems with FDIC insurance: it caps at $250,000 per account and if there was a run, the FDIC doesn’t have the assets to fund the insurance.

Currently, the FDIC has around $9 trillion in insured accounts. A lot of money right? you would think they would have a somewhat comparable value of assets so that if the worst happened, they would get the depositors, or at least a majority of the depositors their money. The problem is they only have $125 billion in assets. So by my math, they could fund 13.8% of accounts. This isn’t to scare you, but just to inform you of the current situation.

So what to do? Take all of your money and stuff it under a mattress?

The phrase “trust, but verify” became famous from Ronald Reagan, who used it when referring to the Soviet Union and their disarmament of the nuclear weapons in their possession. He didn’t invent it though, it is actually a Russian proverb. I like using this phrase when referring to money because if you trust someone to protect your money for you, that is completely fine, but you need to be verifying they are doing it correctly and to your wishes. This can be a bank, credit union, or any type of financial intermediary to which you are granting access to your hard-earned money.

Some practical steps include:

Checking monthly/quarterly/annual statements - take the extra time to make sure they are correct

If you have an interest-bearing account, when is the last time you shopped around? Is your institution still competitive with their rates?

Watch out for bogus/misapplied fees

If using/owning Bitcoin or any other cryptocurrency, use self-custody

Do you have an inordinate amount of money in one place? There is no law saying you or your family cannot have a bank account at more than one bank.

In conclusion, we all work hard for our money and we want to be good stewards of it. Banks are many times an essential and good part of a healthy financial system, and can often help you be a good steward. However, you must stay aware and vigilant when dealing with any financial intermediary because no one will ever care as well for your own money as you can - “trust, but verify”

Life is worth the living, just because He lives,

Trey